The EU’s latest Sustainability Reporting Proposals; A Welcome Simplification… or Unwanted Confusion?

by Tristan Coleman

On the 26th February the EU announced a package of proposals aimed at removing ‘unnecessary’ burden for EU businesses. The so-called ‘Omnibus’ package includes proposals to shake up the Corporate Sustainability Reporting Directive (CSRD) requirements.

Areas such as ‘CSDDD’ (the sustainability and due diligence reporting requirements for the largest corporations), ‘CBAM’ (a carbon reporting protocol for imported goods) and Taxonomy were also addressed in the package but are not elaborated on here.

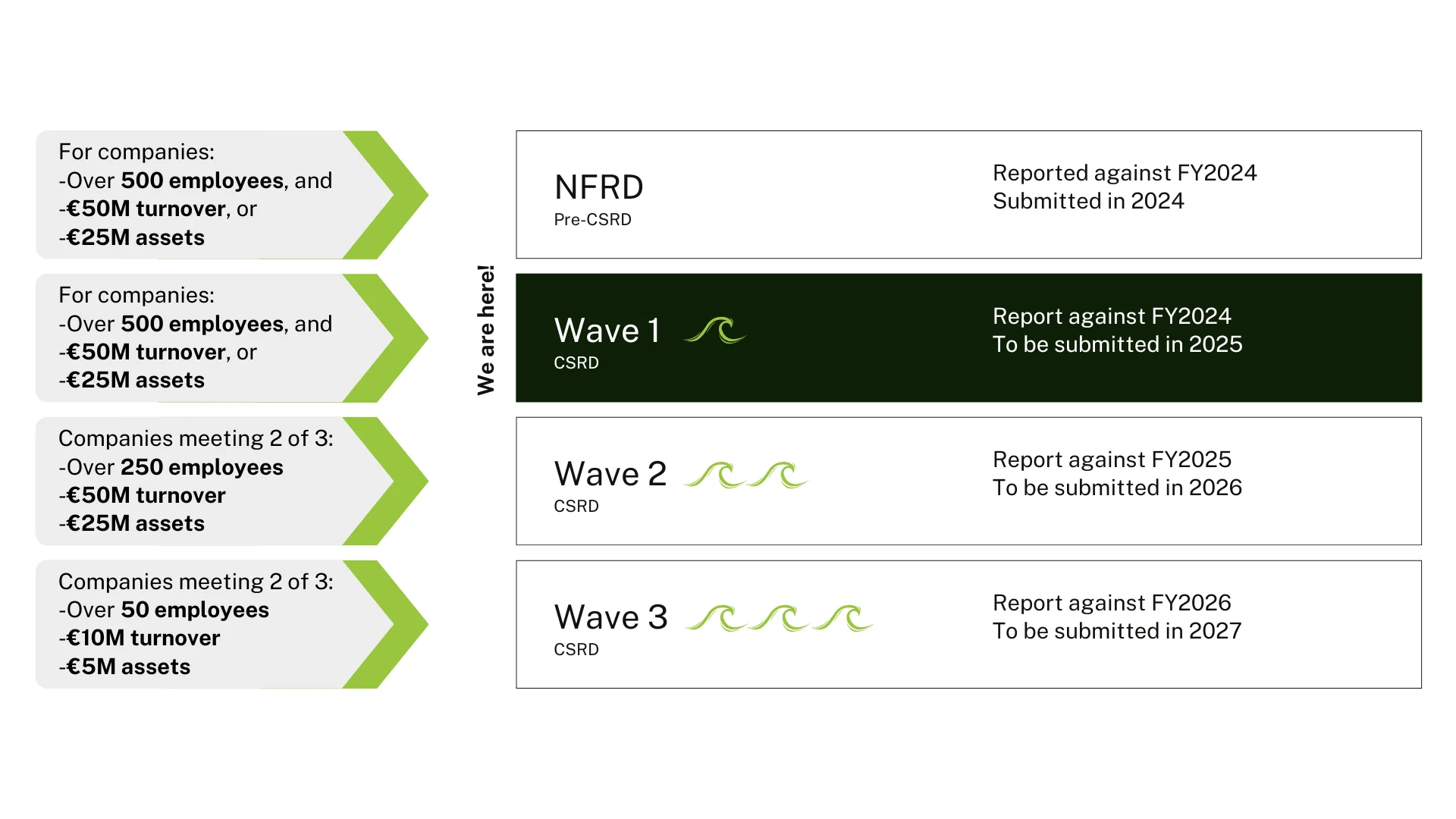

CSRD Scope and Timeline Recap

The Feb 26th CSRD Proposals

Two main legislative proposals have been made with regards CSRD, namely;

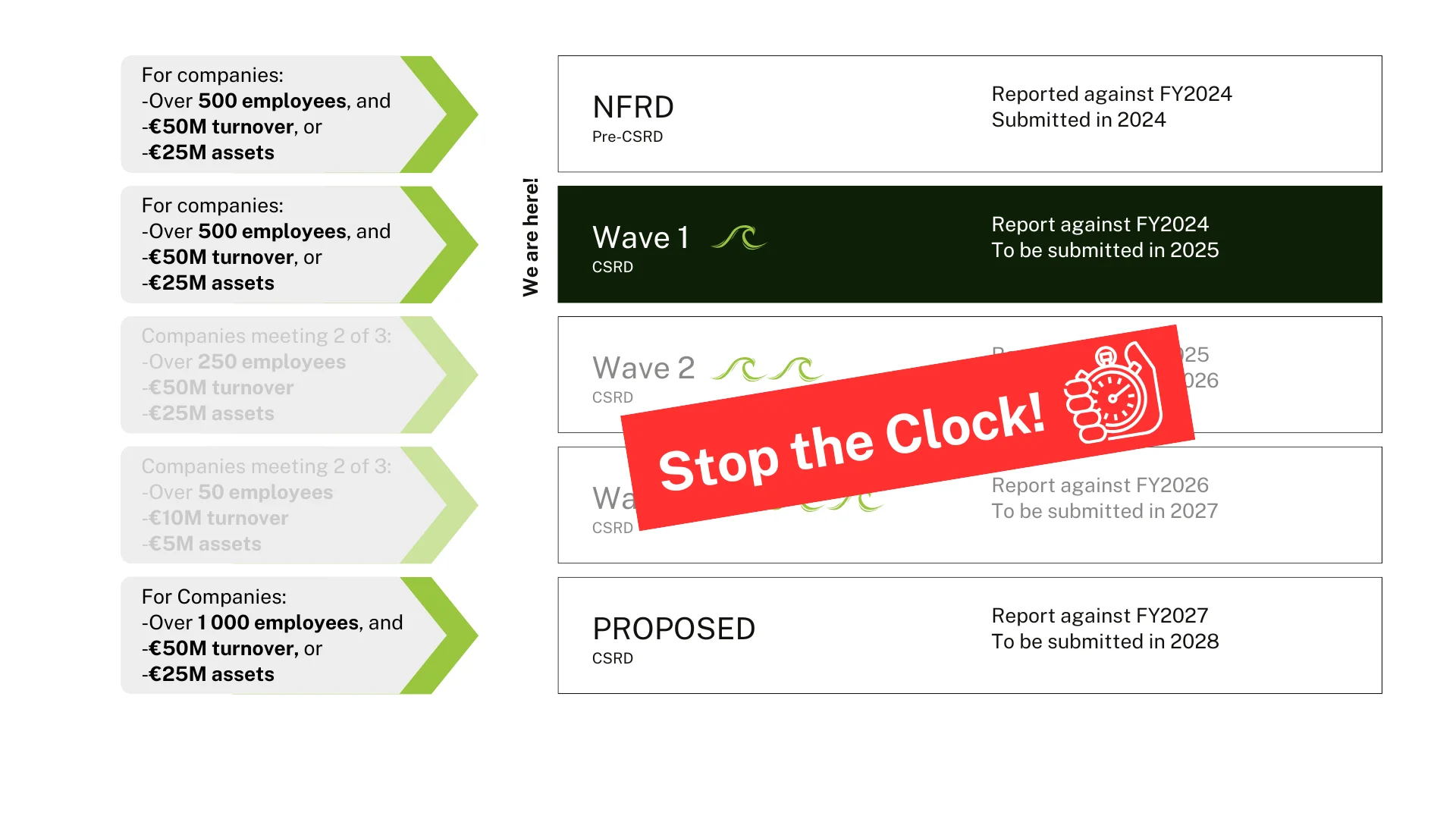

- A ‘stop-the-clock’ proposal postponing the application of all reporting requirements for all of the so called “wave two” and “wave three” companies by two years, and

- A ‘content’ proposal amending the substance of CSRD.

‘Stop-the-Clock’

The package contains a proposal to postpone the application of the reporting requirements for ‘large’ companies and for listed SME’s (so-called Wave 2 and Wave 3 companies). These would be companies that currently fall within the CSRD net but have not yet started reporting (other than voluntarily). The two-year delay is aimed at giving time to the co-legislators to agree to the Commission’s proposed substantive changes.

WKC’s Environmental Law specialist contacted the EU in Brussels for clarification regarding the implications of the proposed delay for companies, including implications for ‘Wave 1’ companies:

“The so called “wave one” companies are subject to existing sustainability reporting rules under the CSRD and have to report in 2025 for financial year 2024. Wave one companies are not covered by the Commission’s “stop-the-clock” proposal.”

Directorate General for Financial Stability, Financial Services and Capital Markets Union, Feb 2025

Content Proposals

Companies that are ‘in-scope’ of CSRD is subject to change under the proposals; those with more than 1 000 employees, and either a turnover of €50M, or assets of €25M being the new criteria.

For those companies that remain ‘in scope’, there a number of proposals aimed at simplifying the substance of the sustainability reports. These include:

- Simplifying the current sustainability reporting standards (ESRS) with the aim of reducing the number of data points;

- Clarifying provisions currently deemed unclear within ESRS; and,

- Deletion of sector-specific standards.

Voluntary Reporting

Under the proposals, companies outside the scope of CSRD may choose to submit voluntarily sustainability reports based on the voluntary standards for SMEs (VSME) developed by European Financial Reporting Advisory Group (EFRAG).

The Commission would adopt the voluntary standard as a delegated act. In the meantime, to address market demand, the Commission intends to issue a recommendation on voluntary sustainability reporting as soon as possible, based on EFRAG’s VSME standard.

“Reports produced on a voluntary basis would not be subject to any audit obligation under the Omnibus proposal.”

Directorate General for Financial Stability, Financial Services and Capital Markets Union, Feb 2025

The VSME ‘Shield’

The proposal will address the “trickle-down” effect upon SME’s in the value-chain of those within the remit of CSRD (and CSDDD), by preventing out-of-scope companies from being subject to excessive reporting requests. This would be achieved through adoption of the VSME-based voluntary standards.

Since this value-chain shield will be desirable to many companies, it is likely that ‘voluntary’ reporting would become somewhat ubiquitous.

The (Long) Road to Adoption

The European Commission’s proposals are just that; proposals.

The legislative process is complex, involving various legislative bodies, themselves consisting of representatives from 27 member states. Moreover, with some political groups and industry representatives likely to oppose the proposed changes, and some groups perhaps even wanting to water-down reporting requirements further, it is difficult to predict what the final outcome will look like.

“Please note that both the Omnibus proposals remain subject to ongoing negotiations and to final agreement by the co-legislators.”

Directorate General for Financial Stability, Financial Services and Capital Markets Union, Feb 2025

The CSRD proposals, if adopted, would need to be transposed into domestic law no later than 12 months from adoption. The ‘stop-the-clock’ proposal would, if adopted, require transposing within just one month from the date of adoption.

What Should Your Business Do Next?

‘Wave 1’ companies will continue with their reporting, although you can expect an updated set of ESRS in due course. The proposed ‘stop-the-clock’ delay would not apply to such businesses.

‘Wave 2 and 3’ Companies planning to report for the first time in 2026 and 2027; there is higher chance that these proposals, if adopted, will offer reprise both in terms of obligation, timelines, and content. Such companies may also benefit from the voluntary reporting protocol with its increased protection for those within the procurement-chain of larger entities. On-going sustainability reporting efforts are, therefore, unlikely to be wasted.

We recommended to ensure that you have a balanced sustainability strategy in place that is cognisant of and able to quickly adapt to potential future changes.

A Step in the Right Direction?

We asked our in-house EU environmental legislation expert, based in Sweden, what these recent Omnibus proposals are likely to mean to the many thousands of businesses across Europe that are impacted by sustainability reporting requirements.

“On the one hand, simplification, but on the other, many more questions! Businesses want certainty. While some reprieve from reporting obligations may be on the horizon, these changes will be met with a mixed reception.

These proposals highlight the importance of having a good sustainability strategy in place. One that not only considers improving and reporting on the sustainability performance of an organisation but also carefully considers the evolving regulatory landscape surrounding it.”

Miriam Markus-Johansson, Principal Environmental Consultant, Gothenburg

We’ll continue to publish more on this topic as we get answers.

Please do reach out in the meantime!

Note: The adoption, transposition status and timeline of the Omnibus proposals, as well as their full content, is not yet known. WKC does not assume any responsibility or liability for any party using this information.